Емец Валерий Николаевич назначен Генеральным директором ООО «Феникс». Решение об этом было принято Федеральным агентством по управлению государственным имуществом (РОСИМУЩЕСТВО), которое выступает от имени Российской Федерации – единоличного участника ООО «Феникс».

В. Н. Емец закончил Николаевский кораблестроительный институт, Академию внешней торговли. Работал в Министерстве морского флота СССР, занимал должности связанные с организацией перевозки грузов. Многие годы проработал в сфере транспортной логистики.

Кадровые перестановки направлены на усиление позиций компании в транспортной отрасли Российской Федерации, сопряжение с планами развития морского, железнодорожного и автомобильного транспорта Санкт-Петербурга и Ленинградской области, осуществление практического взаимодействия всех участников рынка, решение социально-значимых задач для региона.

Дальнейшее развитие портовой и транспортной инфраструктуры, а также техническое оснащение единственного государственного терминала в Санкт-Петербурге особенно важно для поддержания международной торговли, увеличения доли несырьевого неэнергетического экспорта РФ в условиях экономической и политической нестабильности. Для партнеров и клиентов порта это обеспечивает возможность долгосрочного планирования производства и сбыта, а также действенной кооперации в области устойчивого транспорта.

Опыт проектирования, строительства, запуска в эксплуатацию и успешного коммерческого старта ММПК «Бронка» является уникальным и высоко востребованным в современных условиях, в том числе при дальнейшей реализации «Транспортной стратегии Российской Федерации на период до 2030 года».

ООО «Феникс», как оператор ММПК «Бронка», осуществляет перевалку контейнеров, накатных, генеральных грузов и добросовестно выполняет все взятые на себя контрактные обязательства.

Команда ООО «Феникс» во главе с новым Генеральным директором – Валерием Николаевичем Емецем – продолжит работу по повышению эффективности и прогнозируемости бизнеса, усилению сервисных возможностей компании, развитию ключевых для рынка направлений.

ARRC Line is glad to inform you about publishing of "ARRC EUROSERVICES" tariffs in the MAXMODAL Multimodal Network.

You can get them in the ARRC profile. We accept your freight requests via MAXMODAL.

If you have questions, we are ready to answer them in the messenger of MAXMODAL.

Shopping for basic necessities may be a serious problem in 2022 with shortages storming over the most important sectors. Which has been affected the most?

The setup for the product shortages appeared in 2021 and with ongoing constraints, it is not going to ease its grip. However, companies are becoming better at forecasting and trying to make the impact of the skyrocketing demand, the pandemic, and congestion less pronounced. Most of all, tight supplies are expected to affect semiconductors - such big companies as Toyota already report missed production targets - anything that requires aluminum and plastic for production, the food sector, and building materials. With defined pain points, companies will be able to achieve some sort of predictability, however, experts say that 2022 will not be the year when they combat shortages. One thing is to produce necessary products but the other is to have them delivered to the required destination which is an additional riddle to solve. The liner schedule remains under a serious drop since last year when it decreased to 35.8%. Only a few big players managed to keep the rate above 40% with the rest performing rather poorly. Besides, there are incidents that cannot be predicted such as situations when a vessel can run aground like it happened recently with Maersk’s boxship. New legislation contributes to the increased waiting time as well - South Korean ports will be inspecting dangerous cargo with more precision for the sake of safety. Alternatives means of transportation are not the ones to rely on for delivery either as when it comes to roads, surging fuel prices, driver shortages, and increased demand are driving the rates through the roof.

The global community is gravitating to the opinion that the current chaos will last at least throughout 2022, with some predictions going for 2023. Meanwhile, container vessels changing hands are increasing with supersonic speed. Updates report the number of container ships sold last year was 26% higher than the prior record in 2017. This time the number amounts to an insane 1.94 million TEUs. Hence, substantial fleet growth will be the defining trend of 2023 and 2024, and it is the “red-hot” second-hand vessels that will form the majority of it because none of the players wants to waste time waiting for the newly-built vessels. What about congestion? If it does not ease up, there will be 15% more capacity waiting in the queue in the troublesome ports, but the shipping sector acts like it is not its problem with some of the players arguing that overcapacity is not a threat. However, the data proves different - in the Port of LA, the land capacity is 90%, which means that there are too many trucks and people to move around efficiently. Overall, the U.S. ports are responsible for approximately 80% of the global disruption, and many fear the situation getting worse as well as the rates increasing. The shipping sector is at a very vulnerable phase and no wonder that even the big ports are becoming victims of cyber attacks on top of facing all the challenges. The rising costs are resulting in more forwarders setting their carriers and beginning to run their liner services to guarantee space to their customers. In an attempt to increase capacity at the local ports, the Indian government, in turn, is going to develop new cargo terminals in the span of the next three years and aim for the facilitation of multimodal logistics parks. At the same time, DPWorld London Gateway’s expansion has been completed. The overall site capacity increased from 4,000 TEU to 7,400 TEU. Germany is investing in infrastructure as well by planning to contribute 13.6 bn euros to the railway networks.

Apart from contributing to delays, the busy ports are the ones causing the most emissions, and the recent initiative benween the Port of LA and the Port of Shanghai is dedicated to the creating of a green corridor on one of the busiest routes. In addition to decreasing GHG emissions from vessels in the corridor, the partners will reduce supply chain emissions from port operations to improve air quality in the facilities. Another ally may be on the way - Cargotec and Konecranes. The two companies want to merge but it can potentially present problems to the competition, hence, the authorities have not given the green light to the initiative yet. Meanwhile, CMA CGM continues strengthening its presence in the logistics sector by acquiring a 51% stake in the Colis Privé Group.

Lithuania - Belarus ping-pong game is becoming more intense as the latter has responded to Lithuania’s decision to ban transporting Belarusian potash fertilizers through its territory. Stopping trains coming from Lithuania is the first step of the Belarusian response. The country is planning to rely on the internal rail network that it has been investing in during the last several years. Poland has already announced that it will transport its goods to Ukrain through Lithuania, omitting Belarus.

More carriers deploy more capacity as they buy and lease more ships and boxes

It’s seemingly inevitable: As ocean carrier profits soar — and they’re now reaching historic heights — the highly consolidated liner industry will face growing accusations of unfairness and wrongdoing.

The Hill reported Wednesday that Sen. Amy Klobuchar, a Senate Judiciary Committee member, “is working on antitrust legislation related to the shipping industry.” The same day, the watchdog organization Accountable.US accused shipping lines of charging “abusively high fees.”

Social media posts this week alleged that ocean carriers are “profiteering” and “ripping people off.” Over recent months, ocean carriers have been referred to as a “cartel.” In November, Business Insider reported that it received an email from the White House referring to “price gouging by the ocean shipping cartel.”

And yet, the data implies ocean carriers are competing more, not less, with freight prices rising as demand continues to exceed supply chain capacity despite higher carrier competition, not because of artificially lower competition — the definition of a cartel.

Trans-Pacific competition rises

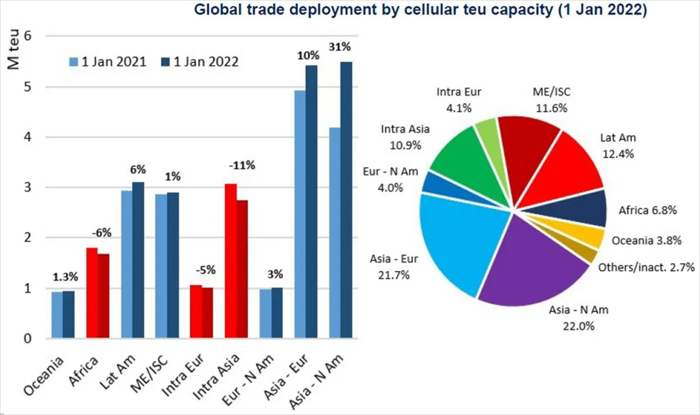

The trans-Pacific is the key trade for U.S. cargo shippers. According to Drewry, Shanghai-Los Angeles spot rates (excluding premium charges) are currently up 152% year on year.

But there are more ships serving the trans-Pacific trade than there were before rates started to surge, and this higher number of ships is being operated by a larger pool of competitors.

According to Gene Seroka, executive director of the Port of Los Angeles, 10 new entrants in the trade served his terminals during the latest peak season.

Alphaliner reported a “massive shift” in carrier deployments in 2021, with 22% of global capacity placed in the Asia-North America lane, making it the largest trade in the world after it stole capacity from other routes. Carriers hiked Asia-North America capacity by 1.3 million twenty-foot equivalent units year over year, “a staggering 31.2% increase.”

Alphaliner said that carriers shifted “as much capacity as possible to the trans-Pacific” to chase “irresistible” rates that were higher per nautical mile (including premiums) than in any other mainline trade.

Alphaliner pointed out that the capacity added to the trans-Pacific far exceeded last year’s increase in cargo volume. Traditionally, that would lead to price competition, yet in this case, excess ship capacity has been soaked up by port congestion.

“The capacity increase was needed to compensate for the huge efficiency loss as many ships faced long waiting times at anchorages,” maintained Alphaliner.

A new report this week from Sea-Intelligence highlighted how the recent era of spiking trans-Pacific spot rates coincides with a sharp decrease in market share of the three carrier alliances (2M, Ocean Alliance, THE Alliance).

In 2012-2020, the trans-Pacific balance was 15%-20% non-alliance and 80%-85% alliance. According to Sea-Intelligence CEO Alan Murphy, “Over the past 18 months, there has been a very substantial increase in the share of capacity offered outside the alliances. We are now at the point where 35% of the capacity offered is on non-alliance services.” The non-alliance share has doubled. Chart: American Shipper based on data source: Sea-Intelligence.com, Sunday Spotlight, issue 549

Scramble for container and vessel capacity

One way carriers supported freight rates in the past was by “blanking” or canceling sailings to artificially limit transport supply (a practice carrier alliances are specifically allowed to coordinate under U.S. regulations). They did so in Q2 2020, when demand abruptly sank due to COVID lockdowns, and they’re likely to do so in the future when demand falls, extending the duration of rate strength.

But over the past year, as freight rates have skyrocketed, carriers have been doing the exact opposite: scrambling to inject whatever vessel and container capacity they can buy or rent into the market. The more ships and containers a carrier has controlled, the more money it has reaped from historically high rates. Virtually any container ship in the world that can float is now in service; the global inactive fleet fell to a fresh low of 2% in mid-January, said Alphaliner.

On the equipment front, containers are ordered at Chinese factories by liner companies or by companies that lease containers to liners. According to data from Drewry, last year’s new container production was by far the highest ever. A total of 7.18 million TEUs of new containers were produced, up 130% from the year before and 62% higher than the previous record set in 2018.

While it can take four months from order to delivery for new containers, it takes far longer — two or more years — from order to delivery for a new container ship. To compete for future market share, carriers went on an ordering spree. Alphaliner told American Shipper that tonnage on order is now 23.3% of on-the-water tonnage. At one point in 2020, it was down to the single digits.

To compete for near-term market share as they wait for their newbuilds, carriers have been leasing and buying ships at an unprecedented pace. Charter rates reached all-time highs last year — with some ships leased for as much as $200,000 per day — and average rates have further increased in early 2022. Meanwhile, a record 1.94 million TEUs traded hands last year in the secondhand sales market.

Another way to bolster near-term market share: Don’t scrap aging ships you otherwise would have. According to Alphaliner, container-ship demolitions collapsed to just 16,500 TEUs in 2021, “well below the 194,000 TEUs recycled in 2022 and a far cry from the 417,000 and 655,000 TEUs demolished in 2017 and 2016, respectively.”

MSC’s capacity had surged by 411,000 TEUs or 10.7% by the end of last year as the company bought over 100 vessels in the secondhand market. In early 2022, additional fleet gains pushed MSC past Maersk and MSC won the title of world’s largest ocean carrier.

Evergreen’s capacity jumped 15.6% last year. Zim’s (NYSE: ZIM) rose 14.9% as a result of charters. Capacity of Cosco, ONE and Pacific International Lines fell.

“Our year-on-year capacity comparison of the top 12 carriers shows major discrepancies between the winners and losers,” said Alphaliner.

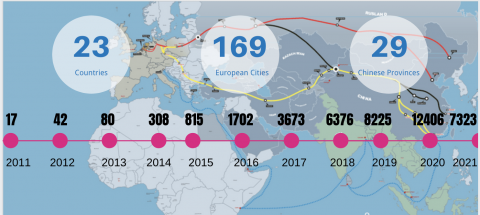

Right before China transitioned into the New Year according to its calendar, it saw another reason to celebrate. On 29 January the 50,000th China-Europe train embarked on its journey towards the west.

According to Xinhua News Agency, the departure of train X8086/5 from Chengdu Chengxiang station marked the magic number of 50,000 trains since the beginning. This

beginning was around ten years ago, when the first China-Europe trains

pioneered across the continents. In the year 2011, a marginal 17 trains were

counted on the New Silk Road.

Doubling every year

This number saw a big boost when in 2013 China’s President Xi Jinping officially

launched the Belt and Road initiative, with the aim of increasing the

connectivity between China and Europe. The train was to play a central role in

this. Over the years, the figures more than doubled every year, and more and more cities

were added to the Eurasian corridor. At present, the China-Europe train reaches

180 cities in 23 European countries. In 2021, the number of trains between

Europe and China amounted to 15,000, a year-on-year increase of 22 per cent.

Quality over quantity

It is going well with the China-Europe train, that is clear for everyone to see. At

the same time, it has been pointed out by many players that it is not all in

the number of trains. The quality of the service must also be maintained, and

the number of trains should be of secondary importance, is a generally held

belief in the industry. This is especially true in the current situation, where the corridor is congested and delays are more frequent than in the years before. Bundling cargo to

make better use of capacity, route expansion as well as infrastructure upgrades

are just some of the solutions at hand.

Морская доставка сборных грузов из Китая в Украину!

+380672456169

Николай, добрый день. Вы можете создать профиль Вашей компании (Zomax Solution Limited), чтобы заводить сервисы, тарифы, откликаться на запросы других участников, а также принимать, размещать заявки и подписывать договоры на отдельные виды перевозок с помощью ЭЦП. В льготный период пока есть возможность воспользоваться всеми функциями бесплатно.

From Germany to Belgium - China is going west, but more activity requires more capacity, which is now equal to gold.

When China announced the major project at the Port of Hamburg, it was only the beginning of its extensive plans to strengthen positions in the EU. Now it is going west towards the Port of Zeebrugge in Belgium, a major asset for maritime logistics, thanks to the freshly extended agreement of COSCO and the aforementioned port. The new strategy will increase port activity which will require additional capacity. Meanwhile, capacity shortage remains a burning issue on intra-Asia routes, which is pushing rates further. Some of the indexes showed an increase from an average of around $500 to $700 per TEU. On the positive side, there are carriers that managed to introduce extra capacity to the Indian Subcontinent and Middle East trades. Indonesia will build a new container port in the Batam Free Trade Zone with a focus on environmental impact. Zim has also reported that it had secured the necessary capacity to meet growing demand and decided to reset its relationship with the 2M alliance.

Overall, the rates’ growth on major Asian indicators had leaped by 780% over the past 26 months; which is forcing industry experts to speak up on the root of it. Liner consolidation remains the top reason. Even the agriculture sector calls for the government to address the unreasonable competition. As for the recent suggestion from the shipping industry to tackle this pressing issue, there was a proposal to introduce a two-year period of notice to allow carriers to use their profits to augment capacity and launch individual services, bringing back more competition. However, the World Shipping Council argues that it should be normalized demand, not regulation, that will solve the supply chain woes. While there are these ongoing debates, the situation will not change and the shipping lines will continue profiting. Although some are against regulations, the congested Port of LA and the Port of Long Beach see the incentives as the means to move empty containers. The new one is supposed to ensure that laden export containers are not deprioritized to make space for empty containers.

Congestion has been a curse for the rail sector too. For example, the one on the Vietnam-China border is causing major disruptions for intra-Asia cargo flows. To address the issue, Alibaba logistics unit Cainiao launched a daily charter flight between Ho Chi Minh City and Nanning, which has provided significant relief and much-needed extra capacity. In addition, land-locked Laos was turned into a land-linked hub that is now serving as a strong alternative to intra-Asia air and ocean freight routes. Besides, Laos railways are cheaper which is a big plus in the current reality of skyrocketing costs. Congestion also disrupted operations of the port of Koper in Slovenia which was devastating especially after it demonstrated spectacular performance a year prior. In 2021, the largest port in the Adriatic region had an annual throughput of 997,477 TEUs.

The Middle corridor is receiving more links too - the new one regards the connection between landlocked Uzbekistan and Azerbaijan to deliver car parts. At the same time, Europe is improving its railweb with Sweden launching a new domestic service as a part of the plan to facilitate further growth above and beyond this in transports on the north-south axis and within Sweden. The initiative aims to switch the old focus on roads to rail as the means to reduce CO2 emissions. There is still a lot to be done to achieve climate targets. Hupac has named three things needed for the European rail to speed up green transition: an energy subsidy for rail, a new bypass on the Rhine-Alpine corridor, and better coordination of construction works. In the coming years, the company is also going to invest 300 million Swiss francs in terminals, rolling stock, and IT systems.

In general, the logistics industry is adopting new technologies to facilitate change. CEVA Logistics offers a wide range of sustainable services that include alternative fuel options, which has caught the attention of Ferrari. Two companies have signed a partnership that serves as an example of how green initiatives are spreading across all sectors.

Source: https://www.porttechnology.org/news/2022-carrier-profits-primed-to-hit-200-billion/

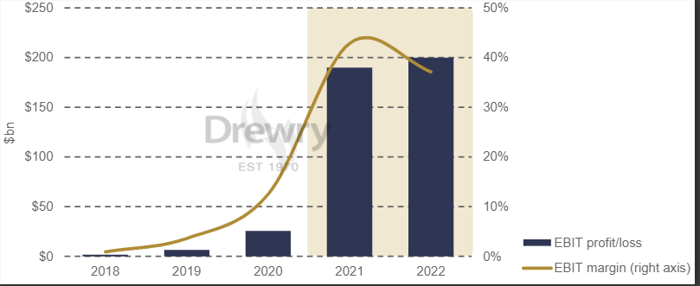

In its latest Container Forecaster report, Drewry anticipates that ocean carriers will ride a third year of 15 per cent or higher in annual growth of total revenue in 2022.

Simon Heaney, Senior Manager of Container Research, wrote that global carrier industry sales are expected to exceed $500 billion for the first time.

The gravy train kept on rolling for ocean carriers in 3Q21 as the industry once again exceeded Drewry’s expectations, Heaney wrote. Shipping lines posted an estimated EBIT performance of $70.9 billion – a nine-fold improvement from $7.6bn in the same quarter a year ago.

Drewry again upgraded its annual operating profits forecast for 2021 from the previous guidance of $150bn to $190bn, at a margin of approximately 43 per cent.

The pandemic and ensuing supply chain crisis is the primary driver of the “supercharged carrier profits and share price bonanza,” Heaney wrote. “In simple terms, the longer the congestion lasts, the longer that freight rates and carrier profits will stay extremely high.

“We think that 3Q21 probably represents the peak quarterly earnings for carriers, but that quarterly results in 2022 will stay on a more even keel that will average out slightly higher. Our revised estimate for this year now stands at $200 billion (margin 37 per cent).”

Carriers are building significant free cash flow that will give them “ample room” to allocate future income to dividends, pay down debt, and pursue growth opportunities, Heaney wrote.

Lines are already beginning to expand portfolios with the extra free cash flow: in December, MSC made a $6.4 billion offer to acquire Bolloré Africa Logistics. The same month, A.P. Moller – Maersk (Maersk) reached an agreement to acquire LF Logistics, a Hong Kong-based contract logistics company in the Asia-Pacific region.

The sky-high earnings for carriers have drawn the attention of regulators – notably earlier in Autumn last year year following a new executive order signed by the Biden administration to crack down on anticompetitive behaviour in rail and ocean shipping industries.

Containers

Fast rising inflation, ongoing supply chain bottlenecks and the Omicron COVID-19 variant are conspiring to slow the pace of growth in container handling, forcing Drewry to lower its year-on-year outlook for world port throughput in 2022 to 4.6 per cent.

The full-year 2021 estimate was also downgraded to 6.5 per cent, from 8.2 per cent.

Full-year 2022 estimates will reach just shy of 900 million TEU in global throughput – although this data is subject to change.