● There has been major ease of Chinese lockdowns. Shenzhen has resumed its work, however, even the several days of disrupted work are going to result in a significant slow down in cargo flow. It may take weeks for it to recover. Trucking has been impacted the most and now as drivers are restricted by sanitary measures, it takes them extra time to operate. This may lead to more queueing ships. The ripple effects are affecting several Northern Ports. After the lockdown in Shenzhen, many carriers including Maersk, MSC, and Hapag-Lloyd had to make schedule changes to avoid congested ports.

● Major delays in the western ports, although updates report the improving situation in the US, are the reason for Indian forwarders as well. Schedule reliability is alarming. CMA CGM is already advising to make network changes since ships deployed on regular services take very long to arrive. There also sailing with no space allocations for loading. As vessel schedules change, cargo carting hours are constantly revised by carriers, at times announced with a shorter gate-in window. However, the Indian situation does not prevent Sinokor Merchant Marine from ordering new ships to increase its capacity on India’s service.

● The Swedish Dockworkers Union has announced to the Ports of Sweden that it will not handle ships going to and from Russia as well as Russian cargo in all ports of the country.

● In contrast to other major players that have suspended operations in and with Russia, COSCO continues its service.

● Truck congestion has resulted from protests in Poland that blocked trucks crossing Poland-Belarus border. Recently, in support of protests, Poland’s prime minister demanded a total block on trade between the EU and Russia. However, these decisions are not made instantly, and for now, Poland is looking for ways to limit Russia’s activity locally.

● Meanwhile, Ukraine bids on rail and calls private companies for investment in railways and terminals that were already in the making to further connect it with the EU.

● Asian lines announce the launch of the new China to India service. The rotation will be Ningbo – Shanghai – Ho Chi Minh – Singapore – Chennai – Visakhapatnam – Port Kelang – Ho Chi Minh – Ningbo.

● More airlines have been shut down due to sanctions. Volga-Dnepr Group shut down subsidiaries that rely on Boeing aircraft.

● COSCO goes for sustainability by exploiting the new pair of 700 teu all-electric ships feeders on the Yangtze in the coming weeks competing with the current world's largest all-electric boxship the Yara Birkeland.

● ONE adds expansion on its agenda too by planning to invest $20bn on new containership and terminal acquisitions over the next eight years. The aim is to improve overall efficiency in slot costs and reduce carbon footprint.

● In addition to its initial objectives to focus on detention and demurrage policies of the big shipping lines, FMC is now going to assess how sufficient the lines serve the US exporters. The commission will be monitoring closely five independent container ship lines that recently entered the market in response to historically high rates shippers are paying for U.S. imports.

● The plan to improve service for shippers also regards the US-grown agricultural commodities. The Northwest Seaport Alliance and the US Department of Agriculture have proposed to preposition containers near the port terminals to enable quick loading on ships.

● With diesel costs accounting for a third of total transport costs, the drastic increase in fuel price has urged the French government to introduce emergency support to local hauliers. They will receive direct aid of $441m which shows that the authorities understand that the road freight industry is key to maintaining the supply chain.

● Houston salvage company Donjon Smit will be responsible for freeing the grounded vessel Ever Forward. However, clearing the ships’ components from mud will not be fast and will take at least a couple of weeks.

● The UK rail freight sector is anticipating the Spring Statement. The industry doubts that the government will do it justice in terms of potential financing, while right now is the crucial moment to invest. The leaders also called to promote a greener railway. The final statement will be revealed shortly and define the rail freight’s development.

● After a stoppage, work in Canadian Pacific Rail has returned to normal, although there are still disagreements that are due to settle.

● Ports of Long Beach and Los Angeles will start collecting Clean Truck Fund fee from April to encourage a change to cleaner trucks and raise resources for the development of zero-emissions technology.

#MAXMODAL #multimodalnetwork #EU #Asia #digitalsupplychain #digitallogistics #ratemanagement #logisticsnews #logisticsandsupplychain #supplychain #sustainability #decarbonisation #containers #containertransportation #containertransport

Good Day!

Dear Colleagues:

Our Transport Company Secure Trans (IE Sona Hovhannisyan) more than 5 years make ocean freight, air freight, and transportation from Asian, European, American countries to Armenia(Yerevan) via Poti and via B. Abbas. We want to find reliable partners for future cooperation. We want to develop our activities and make exports and imports from many countries to Armenia.

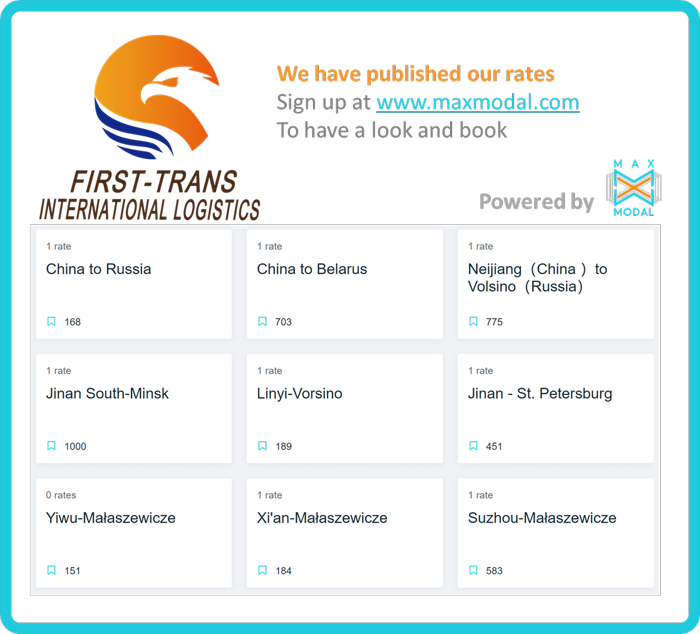

Providers’ rates have been updated on routes China- Australia, Europe, Canada, UAE, Latin America. Please sign in/up to check how competitive your rates are, click «book» to plan your shipments with selected logistics providers ahead, or push a «chat» in case of any questions.

Shipping, clearing and forwarding services.

● Ships are queueing and the wait time keeps growing. Moreover, trucking restrictions are pouring fuel on the fire: no cargo from outside the restricted area can enter Shenzhen. Issues regarding staff availability are also growing due to the fact that people have been ordered to work from home. This results in delays in communication and operations. Warehouses and container freight stations will be closed until at least Sunday. Luckily, the latest updates have reported that the Chinese government will partially lift lockdown in the wake of the collective fear of supply chain disruption.

● However, big companies are still concerned and worried that the impact of the measures will be painful. Hapag-Lloyd is closely monitoring Yantian vessels and expects the COVID crisis to significantly damage its operations in the region.

● All these restrictions are taking a toll on spot rates. The uncertainty about how the situation will unfold has resulted in a rate decline. China - Northern Europe rates have dropped by 4% to 5% with an average price of $12,783. North European exporters have their fingers crossed that rates will fall back to their pre-crisis $2 000 per 40ft. Anticipating the decrease in demand, the 2M alliance is planning more void sailings in the coming month.

● Rates for the US west coast down 7%, to $10,154 per 40ft, and to east coast ports falling by 5%, to $12,276. As for transatlantic, rates were stable at an average of $6 626 per 40ft.

● The trucking industry is under the pressure not only in China. The economic pressure including fuel prices sets it for more turbulence in the US. In the UK, smaller hauliers are calling for the government to take measures and enforce a fixed surcharge rate on customers. Their costs for March are destined to climb 35%. The government's help could ease some of the strain on them. UK haulage companies are implementing emergency fuel surcharges of up to 10% to cover escalating fuel costs.

● One of the factors contributing to the growing prices is a conflict in Ukraine. All modes are under pressure. Seaborne trade with Russia has dropped by 58% resulting in empty store shelves. Rail freight from Russia and Belarus has been halted. Re-routed air cargo is influencing traffic between Europe and Asia. Rail companies have started applying energy surcharges as they can no longer cover the costs due to the risen prices.

● Sustainability comes in handy when it is needed to collect additional surcharges. Ports of LA and Long Beach will begin collecting a rate of $10 per TEU on loaded import and export containers hauled by drayage trucks to encourage the changeover to cleaner trucks.

● While the suspension of operations in Russia and Belarus has hit the industry, carries still have found the alternatives to redeploy intra-Europe tonnage to the region with low capacity, transatlantic routes. For example, MSC launched a new weekly service from the Baltic Sea to US east coast ports. Other companies followed suit. The tension also does not prevent ambitious carriers from ordering new vessels and forwarding fixed long-term charters. CMA CGM has ordered four 7,300 teu LNG-powered ships. Hapag-Lloyd, the 5th ranked by capacity, will take over six 13,806 teu neo panamax ships. Expansion in the number of reefer containers is also taking place. ONE will add 6,500 new reefers to meet the demand for containerized reefer trade, which is expected to continue to grow in 2022.

● Alongside ocean carriers, rail freight forwarders are looking for alternative ways for the China-Europe route that has seen a 40% drop in bookings and its frequency reduced. The Silk Road freight train from Vietnam has been suspended. Among the considered destinations in the southern corridors largely through Kazakhstan, Azerbaijan, Georgia, and Turkey via the Caspian Sea, or Romania via the Black Sea. However, they have long transit times which may result in congestion. Mediterranean ports can be an option, for them, the current situation is the opportunity to come into the spotlight.

● The growing barge delays are forcing some of the ports to call for a task force. The one at the Port of Antwerp will work on ensuring better use of the limited quay capacity.

● New service alert: MSC will operate a new direct service connecting the Port of Gothenburg in the Baltic Sea to the US with a shorter transit time.

#MAXMODAL #multimodalnetwork #EU #Asia #digitalsupplychain #digitallogistics #ratemanagement #logisticsnews #logisticsandsupplychain #supplychain #sustainability #decarbonisation #containers #containertransportation #containertransport

Hi,

This is Joy from First-trans . First-trans Logistics is a company with international multimodel transport company.

What can we do for u?

We provide rail/air/ truck /multimodel transport service, also customs clearance ,door delivery , warehouse service ,etc. (From China to Europe,Russia, Central Asia ect.)

Who are the big companies that we cooperate with?

Our cooperative customers include Midea, Huawei and Green, you can trust us unconditionally.

If you have any questions ,feel free to send message with me.

E-mail: Cottonee19910522@gmail.com

WhatsApp:+86 13548711273

Services that called St. Peterburg iwere operated by COSCO , Maersk , MSC and Samskip , Containerships (CMA CGM), Hapag-Lloyd and X-Press Feeders, stopped all their connections. The number of visits is likely to go down even further when all vessels that were already on their way have discharged their cargoes. Not all carriers are likely to withdraw all their services, as some , like Unifeeder, continues to transport containers . Fewer ships are also visiting Russia’s Far East ports, but the reduction there is much more limited. According to HMM, however, volumes in this trade have declined so much that it is no longer worth calling there. Therefore, it will stop serving Vostochny and Vladivostok (via slots form FESCO). APM Terminals has decided to sell its shares in Russian port operator Global Ports, in which it ultimately holds 30.75% and which it bought in 2012 for USD 173 million. Global ports is involved in four Russian container terminals, FCT and PLP in St. Petersburg, ULCT and Vostochny Container Terminal, and is a partner in Multi-Link Terminals, which operates facilities in the Finnish ports of Kotka and Helsinki.There are two more European terminal operators involved in Russia. These are Eurogate, in Ust-Luga Container Terminal, and MSC’s Terminal Investment Limited, in CTSP . They have so far not disclosed plans for their Russia possessions yet.

First-trans Logistics is a company with international multimodel transport company.

We provide rail/air/ truck /multimodel transport service, also customs clearance ,door delivery , warehouse service ,etc. (From China to Europe,Russia, Belarus,Central Asia ect .)

Good Day Joe, tell me, do you need partners in Russia and Belarus? I represent railway company in Russia. Have you already made tariffs in Maxmodal?

Hi Joy, have you already published your tariffs from China to EU and Russia?

Providers’ freight rates have been updated on routes China- Europe, Japan, and the Middle East. Please sign in/up to check how competitive your rates are, click «book» to plan your shipment ahead, or push a «chat» in case of any questions. MAXMODAL is a neutral digital multimodal network aimed to automate your operations and boost your sales.