Chinese ports are under lockdown again and with the military conflict between Russia and Ukraine, the market is entering another coil of uncertainty and turbulence.

● If it seems like the container market has already seen it all, there is another turmoil to get ready for. Container movement and freight rates quickly reacted to the consequences of the Russian-Ukrainian conflict, and now they are set to react to the lockdown in China that was imposed in 19 provinces. Experts predict that a week-long shutdown of Shenzhen can cause far more disruptions than the notorious Suez crisis because the demand is expected to keep growing. There are also fears that China’s strategy of Covid elimination will be extended to other mainland cities. Due to the reduction in workforces as people are ordered to stay home and limited truck availability, ships are starting to queue at the major Chinese ports. Knowing how they are interconnected with the rest of the international network, the lockdown is going to affect major directions. In particular, India has already reacted. Indian shipping lines are struggling with labor shortages, slowing operations, and vessel turnaround as well as with container shortages because of the lockdown in China. If the situation does not improve, more congestion will be on the way. The importance of Asian presence is visible not only when it comes to congestion. It is reported that Asian shipowners have become the dominant force in global shipping.

● The disruptions caused by Covid and the military conflict are already making Europe to US trade run behind. Sanctioned Russian transhipment cargo from Asia has nowhere to go and keeps piling up. Meanwhile, a shortage of empty containers in Europe results in less equipment available for US exports and carriers that are unable to fill their ships.

● In order to provide sufficient support in medical products, food supplies, and so on for Ukrainian refugees, the terminal in Odesa has started releasing import containers for consignees. Despite the container crisis, many inland storage facilities in Ukraine are offering free storage and cargo-related operations to support civilian needs. While the ocean sector remains highly disrupted, Ukrainian railways show signs of becoming a key player in increasing its exports to the EU.

● More restrictions have been placed on the import from Russia to the US following Russia’s ban to export over 200 products including medical and tech equipment. The US is now prohibiting imports of alcohol, seafood and non-industrial diamonds from Russia. It is also not allowed to export luxury goods to Russia. The measures are destined to pave a way for higher tariffs on a wide range of goods. The EU adds up to sanctions by putting an import ban on Russian steel and iron, a ban on investments in oil companies and the energy sector, and restrictions on the export of luxury items including cars with a value of more than 50,000 euros. In the meantime, HMM suspended its services to the Far East of Russia, although the company has stated that it is due to the market conditions. Market conditions are indeed perplexed with a variety of challenges. Poor schedule reliability and continued delays are fueling the trend of companies starting to charter ships by themselves.

● The crisis is going to be visible across all transportation modes and European hauliers are beginning to worry. In addition to the problem of high diesel prices, another one has appeared. Many automotive components are manufactured in Ukraine and supply disruption will affect the production of trucks. At the same time, the aftermaths of the conflict spill over rail freight traffic between Europe and Vietnam has been suspended for the time being. The crippling increase of costs and drops in sales are happening in the US too, the agricultural sector has become the one that has felt them most prominently.

● The unprecedented chaos in global fuel prices has forced big players to take matters into their hands. MSC is going to review its fuel surcharges fortnightly for all spot and quarterly contracts on Asia trades.

● Major cut off of flights has resulted in some companies deciding to significantly reduce their staff. In the case of Volga-Dnepr Group, it has grounded almost all their aircraft and even the ones with European certification can no longer operate. In response to the EU shutdown, Russia has allowed airlines that lease foreign aircraft to fly domestically which has caused fury in European lessors.

● New routes alert: there is a new multimodal link from Turkey to Germany via France commemorating the increased interest in the Middle Corridor. Spain is about to launch the construction of a railway line to the port of La Coruña. Maersk is going East as well by announcing a call at the King Abdullah Port. Moreover, it has revealed a new cold storage facility in Houston for imports and exports. Also, Maersk is staying true to its green agenda as it becomes the first shipping line that has signed Amazon’s Climate Pledge initiative demonstrating that the shipping sector understands its responsibility and role in cutting CO2 emissions.

#MAXMODAL #multimodalnetwork #EU #Asia #digitalsupplychain #digitallogistics #ratemanagement #logisticsnews #logisticsandsupplychain #supplychain #sustainability #decarbonisation #containers #containertransportation #containertransport

I’m Margarita Rodriguez from 格瑞丰国际货运代理有限公司 (Great full International Freight Forwarding) which provides maritime and air transport services to different countries in America, Europe and Asia, as well as storage service in China. The certification C-TAPT, NVOCC: MOC-NV0684, WCA Membership: 102390, the recognition of the Chinese Ministry of Communication and many satisfied customers can guarantee that our company complies with all the necessary security standards to provide excellent services.

Hoping that my company will be of your interest a I am available for your further assistance

• Email: vivian@wmmqy811815.wecom.work //// 1633373109@qq.com

• Wechat ID:

MAGO202

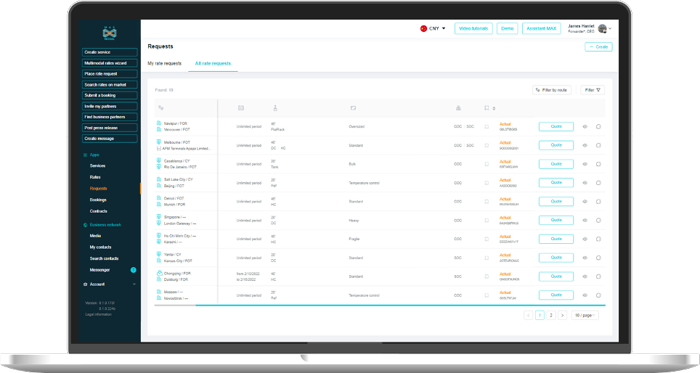

Container freight rates of various providers on routes China-US, China-Canada, as well as India to the European Union, have been updated. Please sign in/up to check how competitive your rates are, click «book» to plan your shipment ahead, or push a «chat» in case of any questions. MAXMODAL is a neutral digital multimodal network aimed to automate your operations and boost your sales.

#MAXMODAL #multimodalnetwork #freightrates #containerlogistics #containertransportation #digitalinnovation #digitalratemanagement #digitalbooking

The Duisburger Hafen immediately ceases all business activities in Belarus. This also includes its stake in the Great Stone Industrial Park.

Who would have thought but in contrast to the predictions that demand will stay elevated, it has started softening, at least on the Asia-Europe trade line.

● The battle for capacity has been replaced with EXCEEDING capacity that carriers are forced to take care of. The first to react among the big players is the 2M alliance by blanking its scheduled loop sailings for the next two weeks. Spot rates, in turn, have also shown a steady erosion. After hitting another high of $15,000 per 40ft at the end of January, they now plummeted to $12,685. However, on the transpacific route, the situation does not change and keeps living up to predictions about the increased demand and tight capacity.

● It is true that every sector on the market has become extremely sensitive to cyberattacks, and MAXMODAL was covering this subject in the past updates. Meanwhile, the notorious trend continues and many fear that in the current context, the logistics chain would be more likely to be impacted by the fallout from cyber-warfare in Ukraine. Among the expected targets are the energy, finance, and operational technology sectors. Experts warn that the impact of the potential cyberattacks can be even bigger than those of 2017 since this time, there is congestion, vessel schedule reliability remains extremely low, and everyone is in the same boat. One attack at a vulnerable target and the domino effect may fall onto many other players. What is also damaging the hope of recovery is the skipped calls to ports. Companies have been using them as a way to manage the capacity of their heavily utilized fleets.

● Russia’s participation in the global trade is too big of a fish to exclude so easily, thus in order to ensure more or less stable partnerships on which so many things from workplaces to delivered goods depend, some countries have started searching for alternative payment ways to ensure shipping’s access to trade. One of them is India where shippers fear already surging rates and potential damage their activity will experience if the sanctions are prolonged. India is one of Russia’s railway partners as well thanks to the important North-South Transport Corridor. The corridor goes through Azerbaijan which recently has upgraded its railways on this route connecting India to Russia. This corridor has a lot of potential as an alternative to the sea shipping route via the Suez Canal. On the contrary, Bangladesh has suspended its shipping to Russia which has resulted in piles of containers at the Port of Chittagong. Apparel factories are also under uncertainty as they do not know if the production for Russian buyers will continue which would be devastating for both sides since Bangladesh has annual trade worth US$1 billion with Russia.

● While some of the freight rates are going down, bunker prices have increased since the beginning go the military conflict between Ukraine and Russia. For the high-sulfur fuel oil, the index rose to $765.93/MT; low sulfur fuel oil has gone up to $1038.07/MT. Some of the companies are self-snctioning Russia and refuse to perform contracts with it, but as a result, they become exposed to contract damages and a big risk of breaching existing commitments.

● The New Silk Road, just like any other important route, has been experiencing a rather turbulent period. However, all the tension has had a positive effect as well. It is reported that congestion has dropped significantly since many companies are omitting Russia and Belarus. For a long while, transit times were more than 30 days, now it is less than 20 days, for example, to Poland. Consequently, new alternative transit routes did not wait long to appear. Germany bypasses Russia through Turkey for cargo from China. Does this commemorate the rise of the Middle Corridor? It is a matter of time, but for now, it has definitely gained its appeal for many western companies.

● In the meantime, Turkey has lost one of the facilities of its Ekol Logistics that has been destroyed during a bombardment in Ukraine. It covers a wide spectrum of transport solutions, and luckily, no was no casualties.

● Despite the difficult situation in Europe, there is still room for new services. At least in Asia. COSCO has announced the launch of a new Daily Express Service between Yantian International Container Terminal and Hong Kong. In addition, the company has celebrated the completion of the Cogent Jurong Island Logistics Hub in Singapore. COSCO has also started a new initiative to build a green port network in the Iberian Peninsula around the ‘dual pivots’ of Valencia and Madrid. China is also pushing on the railway direction and is planning to introduce the second train of the China-Nepal railway service. But the competitors are on the way. Vietnam is developing a non-Chinese outlet for new containers with an annual capacity of 500,000 TEU.

● Sustainability has not left the radar of companies. Maersk has partnered with six companies in sourcing green methanol. The move aims for a faster transition to green energy and decarbonization. The UK has started SHORE green shipping project. Under it, the government is planning to develop the infrastructure to enable zero-emission technologies and power new-age vessels. When it comes to intermodal. Felixstowe breaks a new record in handling containers. Operators are looking forward to maritime work to further increase the ship handling capacity at the port.

An official spokesperson of APM Terminals, said: "A.P. Moller-Maersk, through APM Terminals, owns a minority stake (30.75 percent) of Global Ports Investments (GPI). GPI is an EU company which operates 6 terminals in Russia and 2 in Finland. GPI is listed on the London Stock Exchange. We have today informed our joint venture partners and GPI that we wish to take steps to divest our shares following the invasion of Ukraine and the operational challenges."

Thanks for the comment. changed to FCT. :)

Nice picture of Neva Metal Terminal. It is not Global Ports :) It belongs to Severstal Group

If there is no rate you like, just place a rate request in a few clicks. Upon submission, your request will become available to all users and even to offline providers whose emails you specify. After it, the freight rate you search for will soon become available. Try now. It’s free. Join MAXMODAL. Let’s innovate the future together

#MAXMODAL #RateRequest #EasyRequest #SubmitRFQ #containerlogistics #FCL #MultimodalNetwork #Neutral #Containertransportation

The international rail association UIC has stopped cooperation with its members from Belarus and Russia. This suspension will continue until peace is restored in Ukraine.

33 misfortunes or how congestion has been replaced with the new riddles to solve.

The vulnerable market that hardly recovered from the pandemic and was standing on wobbly legs under the pressure of the congestion has been hit with new challenges. Freshly imposed sanctions on Russia have far-reaching consequences for the whole industry.

● Ship fuel had been unstable for quite some time but the Russian invasion in Ukraine has made its direction very clear: up and up. According to the most recent update, the average price for it has reached almost $900 ($882.50/ton which corresponds to an increase of 73% year on year.) However, even in this unprecedented situation experts predict potential winners - owners with scrubber-equipped vessels. The widening fuel spread will benefit them via substantial fuel-cost savings.

● The effect of the embargo of Russian oil did not omit Kazakhstan crude. Several shipments have been canceled due to the war risk premium associated with the grade of oil. Caspian Pipeline Consortium shares both Russian and Kazakh crude any many companies refuse to go for oil from Kazakstan as there is a risk of it being tainted with Russian ownership.

● The current situation resembles a snowball that keeps growing bigger and the effect of it keeps spreading. High fuel prices (that are also destined to transmit to higher diesel prices) and freight rates paired with Russian airspace now being off-limits to most Western carriers, result in lay-offs of the workforce on the European side as well. At the same time, China-Europe rates climbed more than 80% to $11.36/kg and some companies are already considering implementing a war surcharge on freight shipments. However, the latter will most probably be added to the rate. In addition, flight detours result in a reduction of capacity. So far, it has plummeted by 10% on the Russian market that is still dealing with after-covid recovery just like the rest of the world.

● Inconsistent service and loss of scheduled service got AirBridgeCargo banned from European, US, and Canadian airspace and now the company is desperate to offer its fleet for ad hoc charters. However, it operates in a limited number of regions which will not add up to the capacity loss that the company has experienced, thus the initiative will not last long, according to the experts.

● The issue of the lack of labor force is going to spread across other sectors as well, on land and sea. Seafarers can no longer join and disembark ships freely due to canceled flights due to sanctions. In turn, European road haulage is braced for a growing shortage of Ukrainian lorry drivers. The driver shortage has been one of the most pressuring issues last summer and after it seemed to get better, the situation has fallen down the rabbit hole another time.

● What has also decreased is box shipments into Russia. Updates report that they have fallen by 17% and the trend is going to continue in the aftermaths of the sanctions. The latter has already caused the rise of transshipment dwell times by 43% across all Europe and delayed deliveries to the US due to disrupted suplly chains. Such major players as CMA CGM, MSC, and Maersk have halted their operations in Russia which account for 28% of their activity. All of it will have a direct impact on the further rise of freight rates. The market has already registered rates at $54,000 on Shanghai to Rotterdam route.

● A number of European container terminals have followed suit and suspended all container handling to and from Russia. Overall, container trade has been cut with India, Bangladesh, South Korea, Japan, Thailand, Sri Lanka, and Singapore. Mirroring the decision of major players, Canada has also shut its ports for Russian ships.

● While ocean freight is struggling the most, air freight has prospects of becoming one of the pillars of the long-term business model for the future, despite the turbulent sanctions. At least, this is what the current trend shows. If before, it used to be as means of th last resort, now when everyone is tired of congestion, they start favoring air cargo. Industry leaders claim that it’s no longer a transactional part of our business, but a part of the strategy.

● Have the recent events made everyone forget about the forming shipping monopoly? Hardly. FMC is on the ball to expand its authority for the sale of inflicting the market. It has also voiced out the need for greater funding. The proposed bill immediately faced resistance from the liner community. They continue preaching for every link in the chain doing their part to improve operations and coordination with their service partners and customers. Shipping lines also perceive top-down government mandates as unnecessary.

● The challenging context of the market has delayed Rotterdam’s initiative to launch the Container exchange route amid increasing its container business. The market turned out to be unable to supply such a concept, so it will take time to re-adjust and re-work.