CMA CGM has released updated Freight All Kinds (FAK) rates effective from July 1, 2025, until further notice, but not beyond July 15, 2025.

These rates apply to shipments on vessels departing from all Asian ports, including Japan, Southeast Asia, and Bangladesh, to all North European ports, covering the full range from Portugal to Finland and Estonia, including the United Kingdom.

The new FAK rates are set at US$2,250 per 20' GP container and US$4,100 per 40' GP, 40' HC, or 40' reefer container.

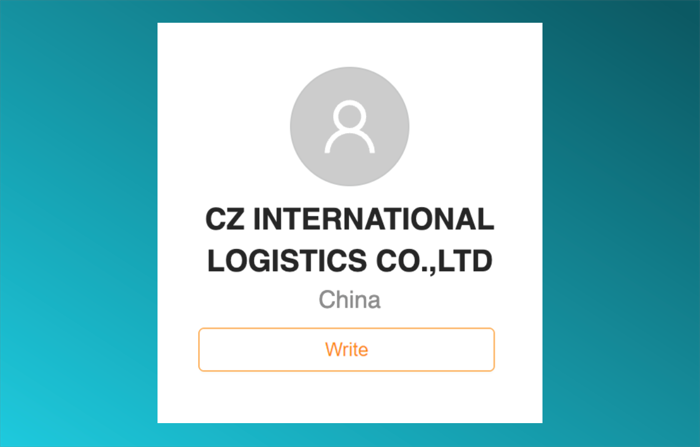

Welcome a new company on MaxModal. You can see CZ International Logistics services on their business profile, drop them a message, add them to your contacts or submit a special request to them

Port of Los Angeles has wrapped up a US$22.7 million restoration project at Berths 177-182, significantly upgrading its infrastructure along the East Basin Channel in Wilmington.

Construction, which began in November 2023 following approval by the Los Angeles Board of Harbor Commissioners two months earlier, involved the development of approximately 382 linear feet of new concrete wharf, 62 feet wide. Additional improvements included slope erosion repairs and the installation of upgraded bollards.

The project replaces part of a timber wharf that was severely damaged in a 2014 fire. The new structure has been built to meet the Port's seismic safety standards, ensuring greater resilience against future incidents.

"This project's completion, especially in the wake of recent devastating fires like those at Eaton and Palisades, underscores the urgent need to prioritize long-term resilience in our rebuilding efforts," said Gene Seroka, Executive Director of the Port of Los Angeles. "We're proud to deliver this critical infrastructure while keeping steel-handling operations running smoothly."

Dina Aryan-Zahlan, Deputy Executive Director of Development at the Port, emphasized the importance of designing infrastructure with future risks in mind. "Fire prevention is a vital component of our operational planning," she noted. "With more than a century of history behind us, modernizing our terminals is essential to staying competitive."

At approximately 1:20 p.m. on 15 June 2025, a newly delivered quay crane tipped over at a non-operational berth at Tuas Port.

No injuries or fatalities were reported, and initial assessments indicate no damage to nearby port equipment or infrastructure.

All operational berths at PSA Singapore remain fully accessible, with port operations and ongoing development works continuing without disruption.

An investigation into the incident is underway. PSA and the Maritime and Port Authority of Singapore are coordinating with the relevant authorities to determine the cause.

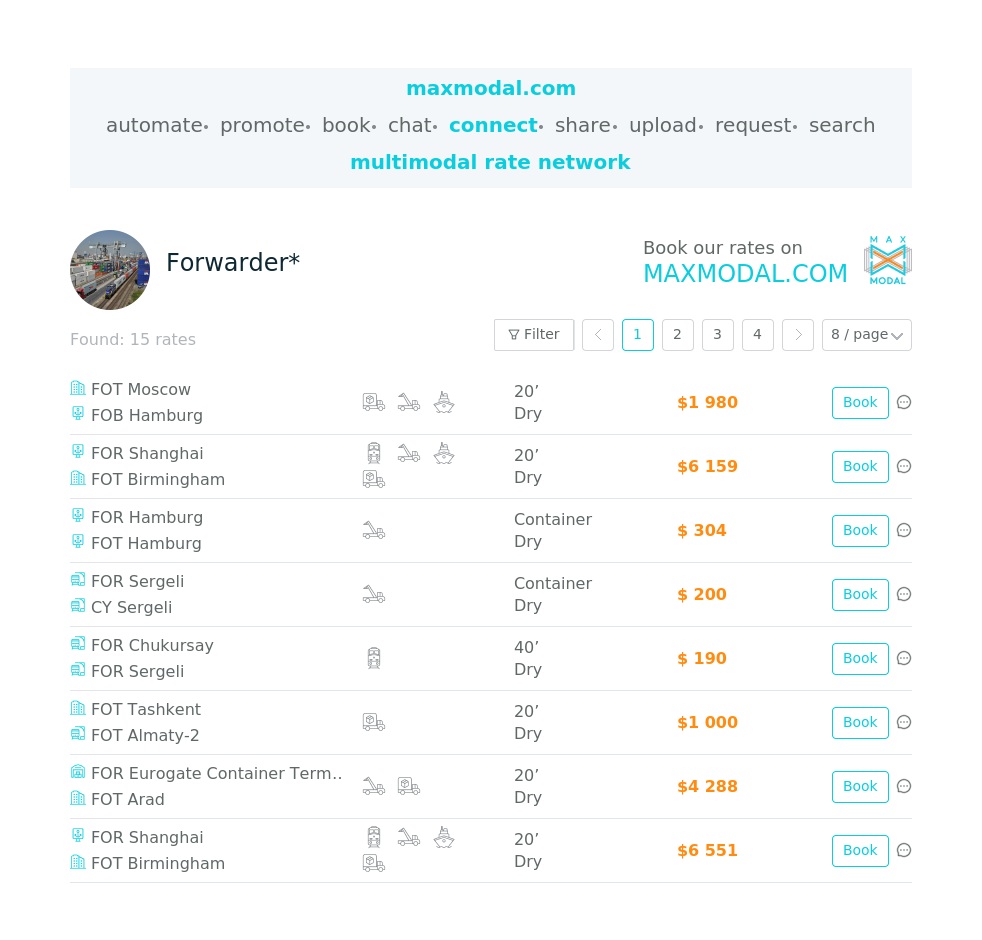

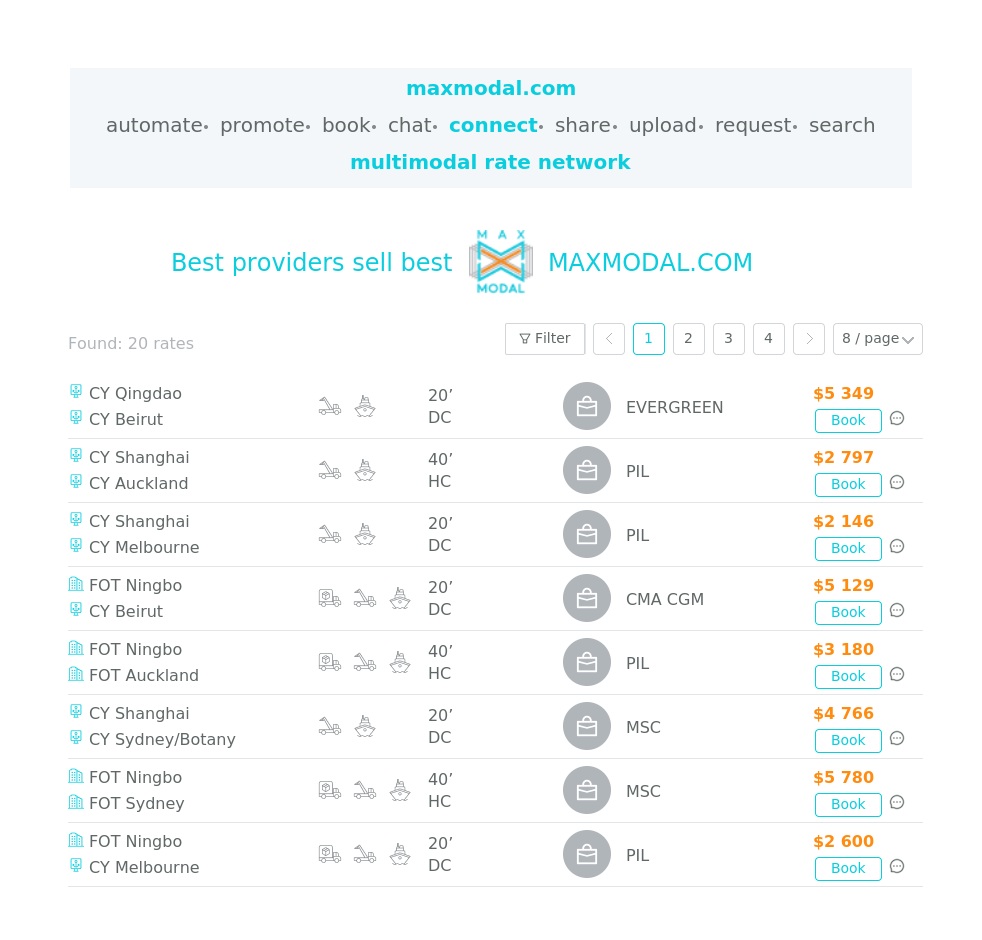

Get the link for freight rates by many providers on maxmodal.com

Transpacific container rates to the West Coast doubled last week on June 1st GRIs to

US$5,488/FEU, with the latest daily rates above US$6000/FEU as shippers start peak season early and frontload goods ahead of tariff pause expirations in July and August.

Prices to the East Coast climbed 60% to US$6,410/FEU with the latest daily rates aboveUS$7,000/FEU, with rates on both lanes about even with levels a year ago when Red Sea-driven capacity restraints combined with an early peak season rush ahead of the ILA port strike threat to push prices up.

Carriers are planning additional transpacific GRIs of US$1,000 - US$3,000/FEU for mid-June and again on July 1st. China's ports are likely still working through some of the backlog of ready-to-ship goods created during the April-May lull in China-US demand.

In addition, some transpacific vessels and equipment that were shifted to other lanes in that period are still making their way back into place.

So as peak volumes for this year's peak season combine with still-restrained capacity and port congestion at several Far East hubs in the near term, much of these June and July rate increases are likely to take.

Get the link for freight rates by many providers on maxmodal.com

Samskip is enhancing its UK trade strategy with a new direct connection offering multimodal options for northeast England.

Samskip has launched a new shortsea container service calling at the Port of Blyth, and linking the UK with other European trade hubs.

This expansion strengthens its presence in northeast England, offering shippers a cost-efficient and sustainable transport alternative that connects to Samskip’s wider European network.

The Blyth service brings direct weekly sailings between Blyth and Rotterdam, fast transshipment to European markets via Samskip’s hub network, and regular departures and reliable transit schedules.

“Expanding to Blyth supports our mission to be closer to our customers and provide agile, multimodal solutions tailored to their evolving needs,” says Samskip Manager Sales & Operations, Scott Montgomery. “This new service opens up exciting opportunities for regional shippers seeking dependable and environmentally conscious logistics.”

This launch represents Samskip’s renewed focus and commitment to enhancing its UK trade offerings. With the addition of Blyth, the company is expanding port options and says it is strengthening service reliability, reaching new customers, and supporting its UK client base with improved access to European markets.

As it invests in this new chapter, Samskip is inviting new and returning customers to rediscover what it can offer — with local care, smarter routing, and the backing of one of Europe’s largest multimodal networks.

The Port of Blyth was selected for its strategic location, modern infrastructure, and growing importance as a regional logistics hub. Its proximity to key industrial zones and ports of entry makes it an important part of Samskip’s UK strategy.

The pause in the US-China trade war, and the associated demand boom, has caused a scramble amongst box lines to inject capacity swiftly, according to Sea-Intelligence, a Danish maritime data analysis firm.

On Asia-North America West Coast (NAWC), the Danish analysts are seeing capacity growth over 30% Y/Y in five of the next 11 weeks.

"If we aggregate it across June/July for Asia-NAWC, then in June, the lines are increasing capacity 12.8% compared to before the tariff pause, and in July, the capacity injection is increasing to 16.5% compared to the pre-pause situation," explain Sea-Intelligence analysts.

Alan Murphy, CEO of Sea-Intelligence, noted that it is an open question whether the tariff-induced volume surge will match this capacity injection. If it does, it can create a significant issue in the ports of Los Angeles and Long Beach, he said.

If the San Pedro Bay ports achieve an 18% Y/Y laden import growth, then the Port of Los Angeles will see June volumes almost at the level seen at the maximum in 2024, while in July, it will face significantly higher volumes than in the pandemic period. Meanwhile, the Port of Long Beach would see new volume handling records for both June and July.